Portugal

-

Moody’s upgrade of Portugal last Friday bodes well for the prospective upgrade of the covered bonds issued by Santander Totta, said analysts on Monday. It should also help to limit covered bond contagion spreading to other lenders, in the event of further negative headlines emerging related to the troubled Portuguese lender, Banco Espirito Santo (BES).

-

Pimco, after staying clear of Portuguese bank or sovereign debt for five years — was in Lisbon recently to investigate opportunities in the troubled peripheral jurisdiction generated by the ongoing Banco Espirito Santo (BES) headlines. The meetings came as several sell-side research analysts tipped Portuguese covered bonds as a good relative value opportunity versus periphery peers.

Pimco, after staying clear of Portuguese bank or sovereign debt for five years — was in Lisbon recently to investigate opportunities in the troubled peripheral jurisdiction generated by the ongoing Banco Espirito Santo (BES) headlines. The meetings came as several sell-side research analysts tipped Portuguese covered bonds as a good relative value opportunity versus periphery peers. -

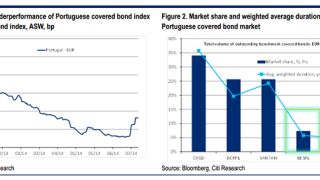

The focus of activity in covered bonds was squarely on Banco Espirito Santo on Tuesday morning with bankers reporting that its one outstanding publicly placed covered bond had widened by 25bp from last Friday. In contrast to the bank’s subordinated debt, which risks being completely wiped out, there is a strong expectation its covered bonds will be fully redeemed on time. However, further mark to market pressure is likely. With Portugal on review for an upgrade, the covered bonds of Santander Totta and CGD present value.

-

Bankers expect more bad news to come out of Portugal and the correction being seen in peripheral covered bonds may therefore have further to go. But this bad news fundamentally does not change the positive longer term picture for the rest of peripheral Europe. A technical retracement had been long overdue and will provide a rare buying opportunity for real money investors and banks looking to cover their shorts.

-

Banco Santander Totta surprised the market on Tuesday, announcing a mandate and setting initial price thoughts for a new five year benchmark of undetermined size.

-

Five Portuguese covered bond deals were upgraded on Friday by Moody’s, in a move that had been widely anticipated following the sovereign upgrade. But the upgrades came against an increasingly volatile credit backdrop which saw some peripheral covered bonds soften as their respective sovereign markets came under pressure.

-

Many Portuguese covered bonds could have their ratings upgraded soon, after Moody’s raised the Portuguese sovereign rating last Friday. Banco Santander Totta’s most recent deal, which is a strong candidate for upgrade, was trading 8bp tighter from last week on Monday, but this was due to ECB rate cut hopes, and not credit upgrade hopes.

-

Credit sentiment is positive, and it seems unlikely that the European Central Bank would take anything other than an accommodative stance at next week’s policy meeting, but bankers are getting cautious that valuations are becoming overstretched, particularly in those markets which have until now been considered safe havens.

-

There was never much doubt that Banco Santander Totta’s first deal since the bailout of the Portuguese government would be a success. The choice of maturity and alluring spread made it an easy choice for the risk-averse and yield hungry. Totta’s first funding in four years attracted one of the largest oversubscriptions and most granular books for a deal of its size.

-

After a four year absence, Portugal’s Banca Santander Totta mandated leads for a three year euro covered bond to be launched on Tuesday subject to market conditions. The short three year tenor was applauded by bankers, who wondered whether the issuer might be able to fund with a double digit spread pick-up over mid-swaps.

-

Investor appetite has shifted to non-national champions, bankers told The Cover on Wednesday, with the window for issuance wide open for lower rated peripheral banks. A Portuguese issuer could step forward soon, one banker said.

-

Moody’s and DBRS have upgraded the Series 1 covered bonds of Portugal’s Banco de Investimento Imobiliario (BII) after they were restructured using a pass through mechanism. The notes will be retained and are designated purely for central bank funding. Parent bank, Banco Comercial Português (BCP), is monitoring the market and, if it were to issue a publicly syndicated deal, it would use its existing programme structured with a soft bullet maturity, said bankers.